Financial Management (FIN 3200 | Weber State)

Chapter 1

- Objective: Maximize shareholder wealth by maximizing fundamental value of stock price

- Money market securities: Mature in less than a year

- Capital Market Securities: Mature in more than a year or not at all

- Four fundamental factors that affect the cost of money

- Production opportunities

- Time preference for consumption

- Risk

- Inflation

Direct: Giving cash for a claim on risky future cash

- Primary market transaction

Investment Bank: underwriter serves as a middleman - Primary market transaction

Financial Intermediary: Savers pay intermediary in exchange for securities of the intermediary.

Financial Instrument: Any claim on future cash flows

Financial Security: A claim that is standardized and regulated

Proprietor

Partner

Corporation

Chapter 2

Indifference Tax Rate

Net Cash Flows

EBIT

(Interest)

(Tax)

NI

+Depreciation

NCF

Free Cash Flows

| NOPAT | |

|---|---|

| NOWC = |

|

| - NIOC | |

| = Free Cash Flow |

ROIC

EVA

Chapter 3

Return: Net Income on Top

Turnover: Sales on Top (Except IT)

Liquidity Ratios

Leverage Ratios

- Exception to turnover rule

Debt Ratios

Profitability Ratios

Market Value Ratios

DuPont

- PM = Return on Sales

- EM = TA/TE (Emory Tate)

- TAT = Sales/TA

Chapter 4

Make a timeline

TVM

N: Number of periods

I/YR: Interest money now would incur per period

PV: Current Value of future cash

PMT: Annuity

FV: Future Value

- Ordinary (end mode) | Annuity due (begin mode)

Uneven Cash Flows

Enter Discount Rate

Enter Cash Flows

Find NPV

Net Future Value

- SWAP from NPV

EFF%

Enter Nominal as I/YR

Enter # of compounding periods as P/YR

Solve EFF%

Amortization

Beg Period, INPUT, End Period, Red, FV (AMORT) - Y

- Principal PMT:

- Interest PMT:

- Remaining Loan Balance:

Make sure N and I/YR are adjusted

Chapter 5

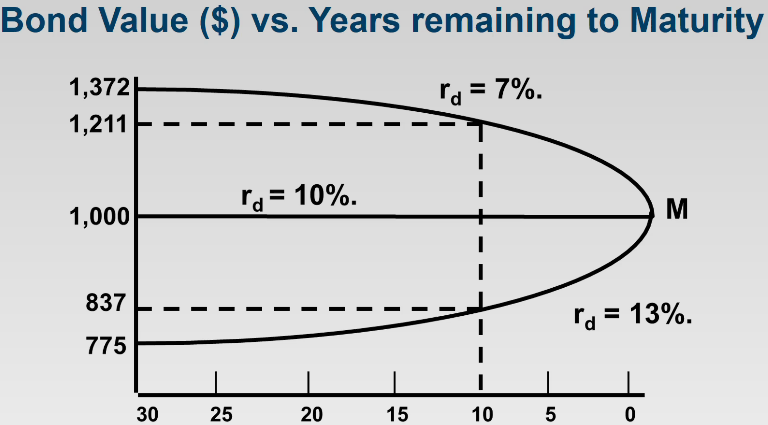

Bond Valuation

- N: Time to maturity

- r: Rate on debt (

), Yield to maturity (YTM), Market, Yield to call (YTC) - PV: (Price)

- PMT: par

Coupon rate - FV: par

1 payment per year, end mode

Bond Yield

Bond Rates

- MRP = Default risk + Liquidity Premium

- MRP only on corporate bonds

- For IP use Average IP though the time period

Bond Price

Use TVM

N

r

Price

Par x Coupon

Par

Adjust for semi annual (N x 2, r/2, PMT/2

Call

Call Period

r

Price

Par x Coupon

Call Price

Expect on premium bonds

Chapter 6

Regression

Enter Values

- x, =, y,

- Mean (Shift 7)

- Stdev (Shift 8)

- Population Stdev (Shift 9)

- Alpha (Shift, 6, SWAP) - b

- Beta (Shift, 5, SWAP) - m

- Correlation (Shift, 4, SWAP) - r

- Goodness of fit =

- Future Estimate (enter X value, orange, 5)

Statistics

Portfolio Analysis

CAPM

Chapter 7

Constant Growth Model

Preferred Stock

Multistage Valuation Model

Cash Flow (HP10bII+)

- Enter

as i/YR - Calculate NPV (Orange, PRC)

Cross out start and finish, used only for calculations

Chapter 9

Component Cost of Debt (

Component Cost of Preferred Stock (

Component Cost of Common Equity (

or- OBY + JRP

Discounted Cash Flows (RE and NS)

Retained Earnings:

New Stock:

Weighted Average Cost of Capital (WACC)

Identify: Target Capital Structure

- Debt

- Preferred Stock

- Equity (Retained earnings or New Stock)

Breakpoint

- Largest capital budget without issuing new stock

Chapter 10

Discount with WACC

Payback

Investment

(Cash Flow)

Repeat

Discounted Payback

Investment

(Discounted Cash Flow)

Repeat

TVM for DCF

- N

- WACC

-

- 0

- Cash Flow

Net Present Value

Enter Cash Flows

Enter WACC as I/YR

Solve NPV

Equivalent Annual Annuity

TVM

- # of periods

- WACC

- NPV

- EAA

- 0

Profitability Index

Internal Rate of Return

Enter Cash Flows

Solve for IRR

Modified Internal Rate of Return

Terminal Value = NFV of future cash inflows

- Enter future cash inflows (no outflows)

- Enter I/YR

- Solve NFV (NPV, SWAP)

TVM - # of periods

- MIRR

- Investment

- 0

- TV

Crossover Rate

Enter Cash flow differences as cash flows

Solve for IRR%

Solve for NPV using IRR as Discount rate to check (should be the same for both)

Chapter 14

Irrelevant: Doesn't matter (can sell or buy for liquidity preference)

Bird in the hand: Dividends are more valuable

Tax Effect: Higher capital gains so taxes are deferred

Clientele Effect: Past policy has determined who bought in the past

Signaling: Increased dividends signal higher expected EPS

Residual distribution Model

-

-

-

Equity Ratio + Debt Ratio = 100%

Repurchase

Calculate Market Cap

($ Repurchase)

/ Market Price

# Shares Remaining

Chapter 16

Set up Relaxed, Moderate, and Tight Policies

Assets

Interest Expense (per policy)

Sales x Policy% = Current Assets

+ NFA = TA

x %Debt = Debt Level

x

Income Statement

Identify EBIT

(Interest)

x (1-TR)

Net Income

Cash Conversion Cycle

- PD = Time from purchase to Cash Outflow

Liabilities

Enter as I/YR

Enter 365 / Costly Time Period as P/YR

Solve for EFF%

or

(D%/1-D%)

+1

^(365/Costly Time Period)

-1

= EFF%