Managerial Accounting (Accounting 2020 | Weber State)

Table of Contents

[[#Introduction]]

[[#Cost Concepts]]

[[#Job Order Costing]]

[[#Cost Volume Profit-Analysis (CVP)]]

[[#Activity Based Costing]]

[[#Budgeting]]

[[#Variance and Standards]]

[[#Short-Term Decision Making]]

Introduction

[[#Table of Contents]]

Accounting Overview

- Accounting: Recording, estimating, organizing, and summarizing financial information.

- Financial Accounting: Reporting to external parties (investors, lenders) using GAAP/IFRS. It is company-wide, precise, and verifiable.

- Managerial Accounting: Provides information to internal users for planning, controlling, and decision-making. It is not mandatory, uses segment reports, and relies on timely, credible judgments, assumptions, and estimates.

Key Functions

- Planning: Establishing goals and developing plans to achieve them.

- Budget: A plan for the future expressed in quantitative terms.

- Controlling: Ensuring the plan is correctly executed by gathering, evaluating, and responding to feedback.

- Performance Report: Compares budgeted data to actual data.

- Decision Making: Selecting a course of action from competing alternatives. It is the most fundamental managerial skill.

Types of Firms

- Retail: Reselling products.

- Service: Providing actions or services.

- Manufacturing: Transforming materials into finished products.

Managerial vs. Financial vs. Tax Accounting

| Aspect | Managerial Accounting | Financial Accounting | Tax Accounting |

|---|---|---|---|

| Requirement | Not mandatory | Required by law | Required by law |

| Users | Internal | External (investors, lenders) | IRS |

| Rules | Best practices | GAAP | Tax Code |

| Time Focus | Past, present, and future | Past | Past |

Key Concepts

- Goal of a Firm: Maximize wealth by maximizing economic profit.

- Opportunity Cost: The benefit forgone by choosing one action over another.

- Sunk Cost: A cost that has already been incurred and cannot be recovered. It should not affect current decisions.

Ethics and Professional Standards (IMA)

- Competence: Maintain professional knowledge, perform duties in accordance with standards, provide accurate and supported information.

- Confidentiality: Do not disclose confidential information, avoid using information for unethical advantage.

- Integrity: Mitigate conflicts of interest, avoid prejudice, avoid discrediting the profession.

- Credibility: Communicate fairly and objectively, disclose all relevant information.

Enterprise Risk Management

- Preventative Controls: Stop harm before it occurs (e.g., authorization, segregation of duties).

- Detective Controls: Detect harm after it occurs (e.g., reconciliation, performance reviews).

Strategy

- Customer Intimacy: Customizing products to fit specific needs.

- Operational Excellence: Providing faster, more convenient, and affordable products.

- Product Leadership: Offering superior products.

Big Data

- 5 V's:

- Variety: Different formats of data.

- Volume: Size or amount of data.

- Velocity: Rate at which data is received and acted upon.

- Value: Resources used to analyze data.

- Veracity: Accuracy of data.

Cost Concepts

[[#Table of Contents]]

Cost Classifications

- Cost Object: Anything for which cost data is desired (e.g., products, departments).

- Direct Cost: Easily traced to a cost object (e.g., direct materials, direct labor).

- Indirect Cost: Not easily traced to a cost object (e.g., manufacturing overhead).

- Common Cost: A cost that supports multiple cost objects.

Manufacturing Costs

- Direct Materials (DM): Raw materials that become part of the finished product.

- Direct Labor (DL): Labor costs directly associated with production.

- Manufacturing Overhead (MOH): All other manufacturing costs (indirect materials, indirect labor, depreciation, utilities, etc.).

- Product Cost: DM + DL + MOH (inventoriable costs).

- Prime Cost: DM + DL.

- Conversion Cost: DL + MOH (costs to convert materials into finished products).

Period Costs

- Selling Costs: Costs incurred to secure customers (e.g., advertising, sales commissions).

- Administrative Costs: General management costs (e.g., executive salaries, office supplies).

- General Costs: Any other non-manufacturing costs.

Cost Behavior

- Variable Cost: Changes in proportion to changes in activity level.

- Fixed Cost: Remains constant regardless of activity level.

- Committed Fixed Costs: Long-term, multiyear commitments (e.g., depreciation).

- Discretionary Fixed Costs: Short-term, annual or less (e.g., advertising).

- Mixed Cost: Contains both variable and fixed elements.

- Relevant Range: The range of activity where cost behavior is linear.

- Irrelevant Range: The range where cost behavior is non-linear.

Decision-Making Concepts

- Differential Cost: Difference in cost between two alternatives.

- Differential Revenue: Difference in revenue between two alternatives.

- Incremental Cost: Additional cost incurred by producing one more unit.

- Opportunity Cost: Potential benefit given up when one alternative is chosen over another.

- Sunk Cost: Cost that has already been incurred and cannot be recovered.

Income Statement Formats

| Traditional Income Statement | Contribution Margin Income Statement |

|---|---|

| Revenues | Revenues |

| - COGS | - Variable Costs (product and period) |

| Gross Margin | Contribution Margin |

| - SG&A | - Fixed Costs |

| Pre-Tax Income | Pre-Tax Income |

Traditional Income Statement

Contribution Income Statement

- Contribution Margin: The amount remaining from sales after covering all variable expenses. It contributes toward covering fixed costs and generating profit.

Cost Estimation

- High-Low Method: Used to estimate fixed and variable costs.

- Total Cost Equation:

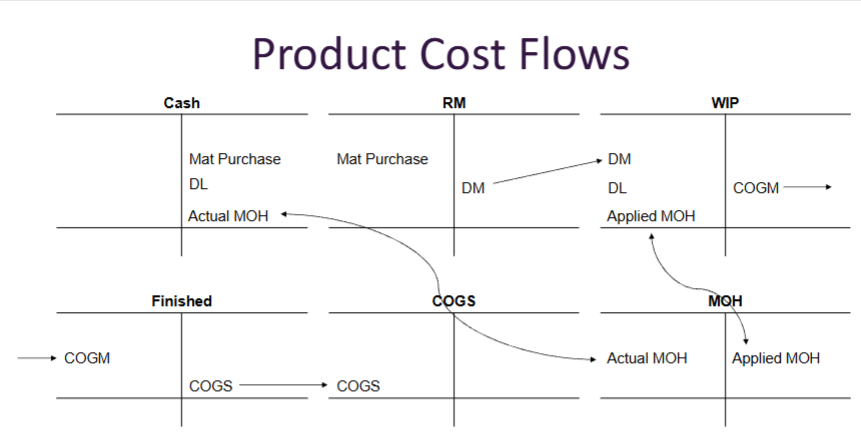

Manufacturing Cost Flows

- Raw Materials (RM): Warehouse inventory.

- Work in Process (WIP): Factory inventory where products are being manufactured.

- Direct materials are transferred from RM to WIP.

- Direct labor and MOH are added to WIP.

- Cost of Goods Manufactured (COGM): Cost of completed goods transferred from WIP to Finished Goods.

- Finished Goods (FG): Inventory of completed products ready for sale.

- Cost of Goods Sold (COGS): Cost of goods sold to customers.

T-Accounts

- Key Equation:

- Key Accounts:

- Cash

- Raw Materials (RM)

- Work in Process (WIP)

- Finished Goods (FG)

- Cost of Goods Sold (COGS)

- MOH Reconciliation

| Cash | Raw Materials | (Warehouse) | Work In Progress | (Factory) | Finished Goods | (Store) | Cost Of Goods Sold | Manufacturing Overhead | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dr | Cr | Dr | Cr | Dr | Cr | Dr | Cr | Dr | Cr | Dr | Cr | |||||

| Material Purchases | Material Purchases | Direct Materials | Cost of Goods Manufactured | Cost of Goods Sold | Actual MOH | Applied MOH | ||||||||||

| Direct Labor | Direct Materials | Direct Labor | Cost of Goods Manufactured | Cost of Goods Sold | ||||||||||||

| Actual MOH | Applied MOH | |||||||||||||||

| Total | Total | Total | Total | Total | Total |

Estimating Manufacturing Overhead (MOH)

- Predetermined Overhead Rate:

- Applied MOH:

- Actual MOH: The real MOH cost incurred during the period.

- Underapplied MOH: When actual MOH exceeds applied MOH.

- Overapplied MOH: When applied MOH exceeds actual MOH.

- Move to COGS:

- Overapplied: Dr MOH, Cr COGS

- Underapplied: Cr MOH, Dr COGS

- Prorate method:

- Use ending balances

- divide each by total for percent

- Times percent by reconciliation

- divide each by total for percent

- To WIP, FG, and COGS

- Use Ending Balance pre-adjustment

- Overapplied: Dr MOH, Cr WIP, FG, COGS proportionally

- Underapplied: Cr MOH, Dr WIP, FG, COGS proportionally

- Use ending balances

Job Order Costing

[[#Table of Contents]]

Overview

- Used by manufacturing firms that produce custom or unique products for specific customers.

- Costs are accumulated by job.

- Suitable for firms producing a few goods for a few customers.

Cost Accumulation

- Direct Materials (DM): Traced directly to each job.

- Direct Labor (DL): Calculated as:

- Manufacturing Overhead (MOH): Applied to jobs using a predetermined overhead rate based on a cost driver (e.g., machine hours, labor hours).

Departmental Overhead Rates

- Overhead costs can be broken down by departments.

- Each department may have its own cost driver and predetermined overhead rate.

- Total applied MOH is the sum of applied MOH from all departments.

Economies of Scale

- Decreasing average total cost as production volume increases.

- Contribution Margin per Unit:

Cost Volume Profit-Analysis (CVP)

[[#Table of Contents]]

What if?

Goal: Maximize Economic Profit

$$ \text{Contribution Margin per Unit} = \text{Price} - \text{Variable Cost per Unit} $$

$$Profit = (P \times Units) - Fixed + (Variable \times Units)$$

$$Profit = Units \times (P - VC) - FC$$

- Use to find break even point

$$\text{Contribution Margin Ratio} = \frac{P-VC}{P}$$

- The amount that goes toward fixed cost

= Amount that goes toward variable cost

$$Profit = (Rev \times CMR) - FC $$

Margin of Safety

$$ \text{Safety Margin} = \text{Revenue

} - \text{Break Even Revenue}$$

Operating Leverage

$$\text{Operating Leverage} = \frac{\text{Total Contribution Margin}}{Net Income} $$

- High: lots of fixed costs

- Specific to time period

Activity Based Costing

[[#Table of Contents]]

When?

- Lots of product diversity

- Costs are not unit-level

- Complex manufacturing process (high overhead cost)

- Low data processing cost (collecting and using)

- Some products have a higher margin

- Actions do not seem to align with competitors

- Line managers no not believe costs

- Complex products are very profitable but not priced at a premium

When the benefits outweigh the costs

- Costs:

- More complex calculation

- More complex data collection

- Change of culture

- Benefits

- More accurate costing

- Better ability to properly set prices - especially when costs are large

Cost Pool: Uses it's own cost driver and rate

Can be used for only MOH or applied to SG&A

- What are they using it for?

Guide to Activity Based Costing

- Define Activities and Identify cost driver (drivers are unique)

- Assign budgeted costs to cost pool and calculate budgeted cost driver

- Calculate budgeted rate

- Assign cost (applied ABC)

$$ \text{Activity Rate} = \frac{\text{Budgeted Cost}}{\text{Budgeted Driver}}$$

How do costs vary depending on cost drivers?

- Units

- Hours

- Customers

- Batches

- Products

First stage allocation

- Assign all costs to different pools (Budgeted Cost)

- Does not need all product costs

- Assign an Activity Measure (Budgeted driver)

- Correlated with cost

- Easy to measure accurately

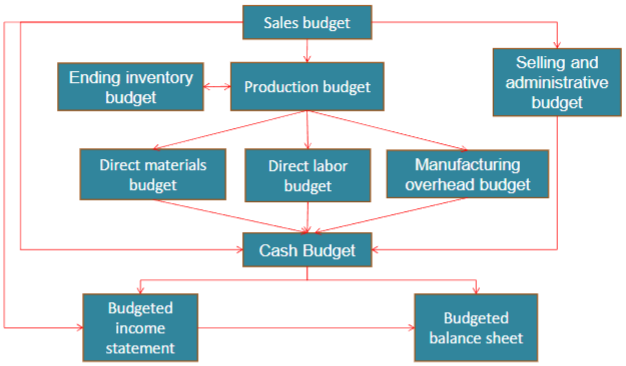

Budgeting

Planning Budget

Flexible Budget- Reworking the planning budget to the actual level of sales

- Budgets may not be the same

- Actual Units

Standard Costs and Usages

Actual Budget - Actual Units

Actual Costs and Usages

Plan

- Developing goals and preparing budgets to achieve those goals

- Make goals

- Plan how to meet goals

- How to allocate scare resources

- Foresee problems

Control - Gathering feedback to ensure that the plan is being properly executed or modified as circumstances change

- Coordinate across divisions

- Create evaluation benchmarks

Perpetual budget: Creating a budget that rolls forward as it's completed

How

Top-Down

- Top managers set budgets - Big picture

- Advantages

- Sets expectations

- Can push lower management to improve

- Often improves coordination

- Disadvantages

- May not get "buy-in"

Bottom-Up (Participative)

- May not get "buy-in"

- Lower managers set budgets, then all are compiled

- Advantages

- Buy-in

- More Accurate

- Disadvantages

- "Slack" (easy goals)

Cost Function:

Avoid

- Too Easy

- Too Hard

- Conflicting Goals

Production Budget

- Goal: How many units to make

- Selling

- Ending FG

- (Beg FG)

DM (Material Purchase) - Using

- Ending RM

- (Beg RM)

DL - Using

- Overtime

MOH - Based on cost driver

Cash Budget

- Beginning Cash

- +Cash In

- Cash Available

- (Dispersements)

- Net Cash

- +Loan

- Ending Cash

Income Statement: Units to sell (not to make)

- Cash flows are what's made

Variance and Standards

[[#Table of Contents]]

Budgets as a control

- Beyond planning, budgets are used to verify that goals are met

- Compare results to plan

- Explain why they differ to make better future plans

Variances

Documentation of differences between budgets and results

- Always a positive number (labeled as Favorable - F, or Unfavorable - U)

Activity Variance: Difference in sales output

- Planning - Flexible

- Cross out Actual

- Memorize: Activity ignores Actual

Spending Variance: Difference in cost or usage - Flexible - Actual

- Cross out Planning

- Memorize: sPending ignores Planning

Favorable: Lower cost (or cost driver) or higher revenue

Unfavorable: Higher cost (or cost driver) or lower revenue

Standards

- What should go into making a product

- Standard Usage: Unit Quantity of material, labor, machine hours, etc.

- ? / Unit

- Production

- Standard Cost: Cost of one unit of what is being used (1 pound, 1 hour, etc.)

- $ / Unit

- Purchasing

Standard UsageStandard Cost = $ / Unit

Ideal Standards (perfect)

- Pushes managers to improve

- Standards will likely not be met

Normal Standards (average) - Attainable

- May not lead to fast improvements

All standards come from past data

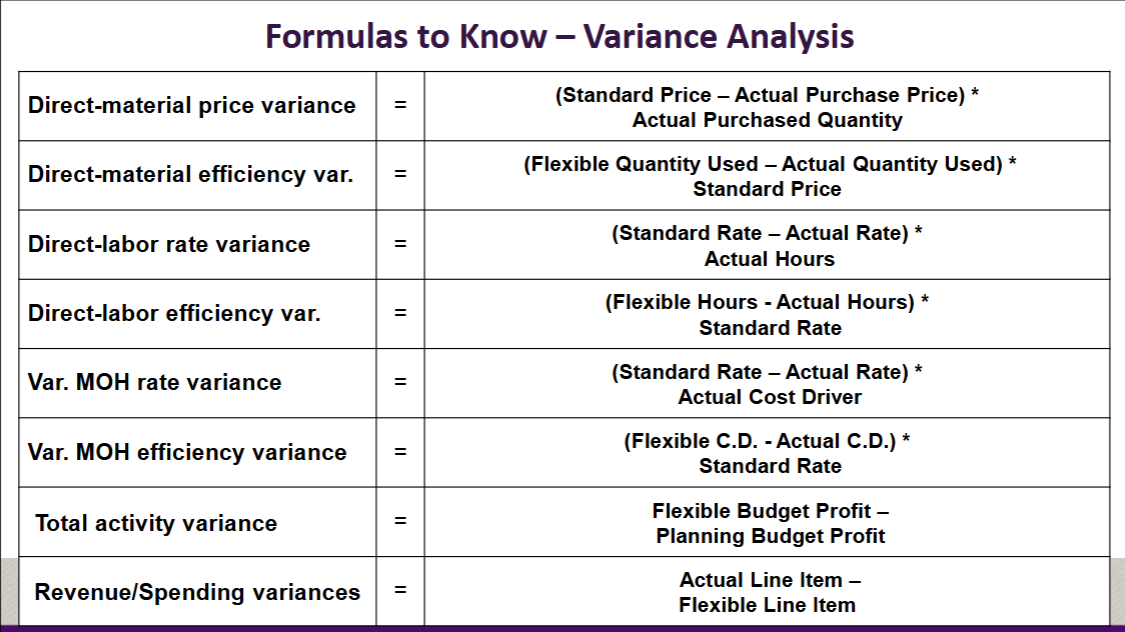

Efficiency and Price Variance

Efficiency Variance = (Actual Usage - Flexible Usage)

- Standards come from planning budget

Price Variance = (Standard Price - Actual Price)Actual Purchases - Price per unit

- Purchases will not always equal usage

Efficiency Variance + Price Variance = Total (DM, DL, etc.) Variance

Total ( ) Variance = Spending Variance

Standard Quantity

$$Units \times \text{Quantity per Unit} $$

Standard Cost

$$\text{Standard Quantity} \times \text{Standard price} $$

Spending Variance

$$\text{Actual Cost} - \text{Standard Cost} $$

- Favorable if Standard > Actual

- Also called cost variance

Cost Variance

$$(\text{Actual Price} - \text{Standard price}) \times \text{Actual Quantity} $$

- Favorable if Standard > Actual

Efficiency Variance

$$\text{Actual Quantity} - \text{Standard Quantity} $$

- Favorable if Standard > Actual

- Also called Material Quantity Variance

Chapter 7 - Activity Based Costing

[[#Activity Based Costing]]

ABC Costing

- When to use ABC vs Plant-Wide rates

Calculate Activity Rates

- ABC

- Traditional

- First Stage Allocation (cost / driver)

- Getting the $ into the pool

- Second Stage Allocation (jobs / product)

Rate = Cost / Driver

ABC Rate = What changes / The thing that changes it

Chapter 8 - Budgeting

[[#Budgeting]]

What is the goal of the budget?

Why Budget

- Planning and Control

How - Top Down

- Participative Budgeting

- Pros and Cons

Production Budgets

- Units to Manufacture

- DM to Purchase

- DL to Purchase

- Variable MOH Expected Expense

Flow of Budgets

- Sales Forecast to Revenue Budget

- Revenue to Purchases Budget (or Production Budget)

- Cash Budget

Planning Budget (Income Statement)

Chapter 9 - Flexible Budgets

Making a Flexible Budget

- Actual

Standards

Creating Standards

- Ideal vs. Practical (Ch. 10)

- Standards may use cost functions (TC = FC + VC * Activity Measure)

Activity Variance

- Planning vs Flexible

Spending Variance (Revenue)

- Actual and Flexible

Chapter 10 - Standards

Spending Variances

Price and Efficiency (Volume) Variances

- Direct Labor, Direct Materials, Var. MOH

- Remember inventory issues for DM

- Know how to calculate and interpret variances

Workout: Forward Multiple Choice: Backward

Is the spending variance due to price or quantity

- Line by line

Formulas

Short-Term Decision Making

[[#Table of Contents]]

Forecasting is an Art.

Mechanics of Decisions is a Science (focus of chapter).

Good Decisions

- Identify Options

- Forecast Consequences

- Make Profit Maximizing Choice

- Watch out for Constrained Resources

Everything Method

- Identify All Costs and Benefits to each option

- "Pro-forma" (budgeted) income statements

- Choose the biggest Income (lowest cost)

- Pro: Already have income statement

- Con: Includes less relevant data

**Relevant Cost and Benefit Method

(Method used in class)

- Identify Options.

- Dismiss Irrelevant costs and benefits.

- Good Idea to keep variable costs to give an accurate Contribution Margin

- Identify relevant (differential) costs and benefits of each option.

- Pick profit-maximizing option.

- Identify net benefit.

- Pro: Cannot always get projected income statement, Including irrelevant costs may distract.

- Cons: May not give the full picture, even if the decision is the same.

- Better to include irrelevant info than disregard relevant info.

Relevant: a result of choosing an option

- Best to examine what changes

- Opportunity cost is relevant

Irrelevant: Anything that stays the same with all options

- Sunk costs is generally irrelevant

- Fixed costs may be irrelevant

Capital Budgeting

Tax savings due to depreciation

- In Class: Straight Line Depreciation and Single Tax Rate

- In reality: MACRS (accelerated) depreciation and Graduated tax rates (incremental tax brackets)

Profitability Index

Financial Statement Analysis

- Compare data within a company over time

- Compare data across companies

Garbage In, Garbage Out

Ratios

- Valuable, but often don't tell the entire story

Analysis

Vertical Analysis (Apples to Apples)

Change everything to percentages

- Balance Sheet = % of Assets, Liabilities, Equity

- Income Statement = % of Revenues

Horizontal Analysis (Timeline)

Look at the company though time

Change everything to