CLEP Microeconomics

Table of Contents

- [[#1. Basic Economic Concepts (10-16% of exam)]]

- [[#2. 2. Supply and Demand (15-20% of exam)]]

- [[#3. Theory of Consumer Choice (5-10% of exam)]]

- [[#4. Production and Costs (10-15% of exam)]]

- [[#5. Firm Behavior and Market Structure (25-33% of exam)]]

- [[#6. Factor Markets (6-12% of exam)]]

- [[#7. Market Failure and Role of Government (8-14% of exam)]]

- [[#Formulas]]

- [[#Exam]]

1. Basic Economic Concepts (10-16% of exam)

The study of how people allocate scarce resources

Production Possibilities Curve (PPC)

- Shows maximum output combinations with given resources in a snapshot of time

- Points on curve = efficient; inside = inefficient; outside = impossible

Comparative Advantage and Trade

- Law of Comparative Advantage: Difference in relative costs of production are key to determining patterns of trade

- Comparative Advantage: Lower opportunity cost in production

- cannot have comparative advantage for both goods

- Absolute Advantage: Higher productivity/efficiency

- Specialization and trade leads to higher consumption for both parties

- Self Sufficiency: Producing everything for yourself

Economic Systems

Systems of production, allocation, exchange, and distribution

- Market Economy: Private ownership and allocation (capitalism)

- Property Rights: Essential for market economies, ability to own (use, earn, transfer and enforce rights)

- Command Economy: Government ownership and allocation (communism)

- Market Socialism: Planned ownership, Private allocation

- Property Rights: Legal framework for ownership and resource allocation

Marginal Analysis

Costs and benefits of one additional unit

- Profit Maximization:

- Produce where Marginal Revenue = Marginal Cost

- Vise versa for factors of production (labor)

- Consumer Maximization:

2. Supply and Demand (15-20% of exam)

Market Equilibrium

- Equilibrium: Where supply and demand curves intersect (

, ) - The invisible hand will pull toward this equilibrium

- Surplus: Price above equilibrium; quantity supplied > quantity demanded (floor)

- Shortage: Price below equilibrium; quantity demanded > quantity supplied (ceiling)

- Perfect Competition: we assume perfect competition - many buyers and sellers, identical goods, no barrier to entry or exit, perfect access to information, no externalities, no single agent is able to exert price control.

- firms are price takers

Demand

- Comes from Buyer

- Shifters: Income, Preference, Related goods, Number of buyers, Future expectations

- movement caused by change in price. Usually from changing supply

- Negative slope: consumers buy when MU = MC, decreasing marginal utility and variable consumer utility leads to a negative Demand Slope (Schedule).

- Compliments: consumed together. (negative cross price relationship)

- Substitutes: consumed instead. (positive cross price relationship)

- Normal Good: Increased demand when income rises

- Inferior Good: Decreased demand when income rises

Supply

- Comes from Seller

- Shifters: Production costs, Technology, Number of sellers, Government regulation, Future expectations

- movement caused by change in price. Usually from changing demand

- Positive slope: producers supply where MR = MC. they supply more when they can charge more (greater marginal revenue)

Price Controls

Government set limits

- Binding: Interfere with equilibrium

- Price Ceiling: Maximum legal price. (Rent control)

- Creates a shortage because

is higher at the lower price, and is lower

- Creates a shortage because

- Price Floor: Minimum legal price. (Agriculture Support)

- Creates a surplus because

is higher at the higher price, and is lower

- Creates a surplus because

- Binding: Controls that affect equilibrium

Elasticity

How much does quantity respond to price change

- Price Elasticity:

- Percent Method:

/ - Midpoint Method:

/

- Percent Method:

- Elastic: |Ed| > 1 (responsive to price changes)

- Inelastic: |Ed| < 1 (less responsive to price changes)

- Income Elasticity: Distinguishes normal from inferior goods (replace price with Income)

- Positive = Normal good. Negative = Inferior good

- Cross-Price Elasticity (

): Determines substitutes vs. complements - Positive = Substitute. Negative = Compliment. |

| > 1 (strong correlation)

- Positive = Substitute. Negative = Compliment. |

- Elasticity is not determined by the graph, but by where on the graph you are

Welfare Economics

- Consumer Surplus:

. Area below demand curve, above price - Producer Surplus:

. Area above supply curve, below price - Total Surplus:

- Equilibrium maximizes total surplus (allocative efficiency)

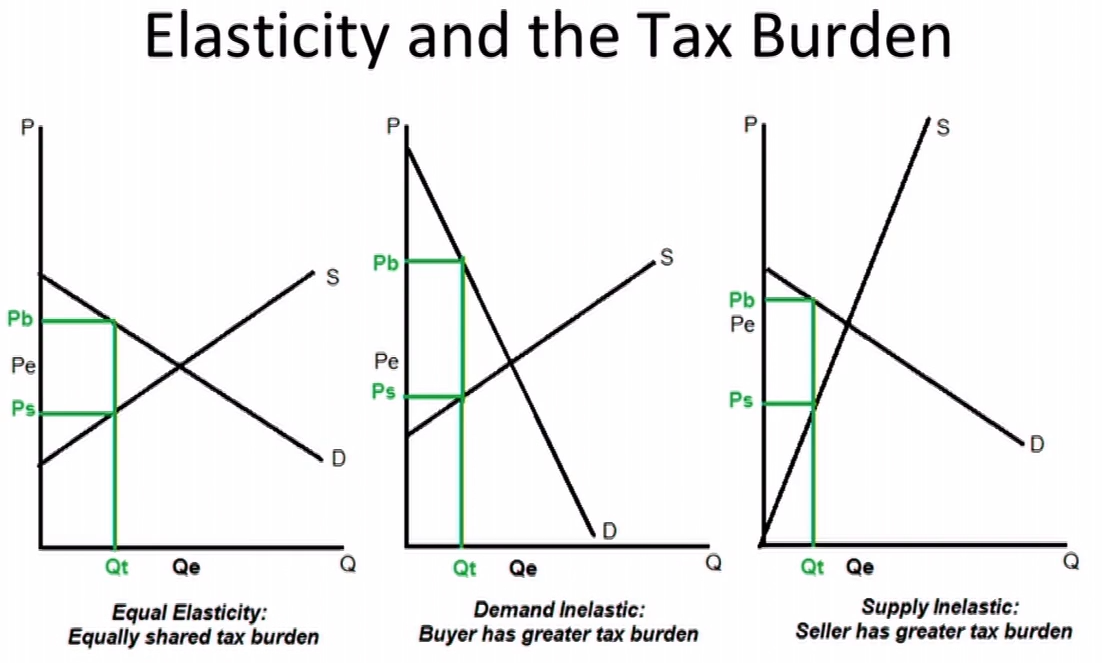

Taxation

- Creates wedge between price paid by buyers and received by sellers

- Tax Burden: Split based on relative elasticities. More elasticity = greater burden

- Deadweight Loss: Efficiency loss from taxation

- Tax Revenue = Tax × Quantity (after tax)

3. Theory of Consumer Choice (5-10% of exam)

Utility Theory

- Total Utility: Total satisfaction from a given quantity (Parabolic)

- Total utility maximized when

(x-intercept)

- Total utility maximized when

- Marginal Utility: Additional satisfaction from one more unit (Usually linear in examples)

- Diminishing Marginal Utility: MU decreases as consumption increases, even into negatives

Consumer Optimization

- Budget Constraint Curve: Shows all affordable consumption combinations

- Equimarginal principle (Utility Maximization Rule):

- Consumer equilibrium: where budget is fully spent and the equimarginal principle is met

- The Consumer Demand Curve: comes from the optimal bundle at each price

- Market Demand Curve: the sum of all consumer demand curves

(Continue From Here) Income and Substitution Effects

- Income Effect: Change in consumption due to change in purchasing power

- Substitution Effect: Change in consumption due to relative price changes

- Both effects work together when prices change

- Help explain downward-sloping demand curves

4. Production and Costs (10-15% of exam)

Production Functions

- Short Run: At least one fixed input (usually capital)

- Long Run: All inputs variable

- Total Product: Maximum output from given inputs

- Marginal Product: Additional output from one more input unit

- Diminishing Returns: MP eventually decreases as input increases

Cost Concepts

- Fixed Costs (FC): Costs that don't change with output

- Variable Costs (VC): Costs that change with output

- Total Cost (TC): FC + VC

- Marginal Cost (MC): ΔTC/ΔQ

- Average Costs: AFC = FC/Q, AVC = VC/Q + ATC = TC/Q

Cost Curve Relationships

- MC intersects AVC and ATC at their minimum points

- When MC < ATC, ATC is falling

- When MC > ATC, ATC is rising

- AFC always decreases as output increases

Long-Run Costs

- Economies of Scale: ATC decreases as output increases

- Constant Returns to Scale: ATC remains constant

- Diseconomies of Scale: ATC increases as output increases

5. Firm Behavior and Market Structure (25-33% of exam)

Profit Maximization

- Economic Profit: Total Revenue - Total Economic Costs

- Accounting vs. Economic Profit: Economic includes opportunity costs

- Profit Maximization Rule: Produce where

- Shutdown Rule: Continue if

(short run)

Perfect Competition

Characteristics:

- Many buyers and sellers

- Identical products

- Free entry and exit

- Perfect information

Behavior:

- Firms are price takers (P = MR)

- Short run: Can earn profits or losses

- Will incur losses if

- Will incur losses if

- Long run: Zero economic profit

- Allocatively efficient when

Monopoly

Characteristics:

- Single seller

- Barriers to entry

- Price setter

Behavior:

- Profit maximization: MR = MC, charge price from demand curve

- P > MC (allocatively inefficient)

- Creates deadweight loss

- Can earn long-run economic profits

Sources of Monopoly Power:

- Resource ownership

- Government-created monopolies

- Natural monopolies

Oligopoly

Characteristics:

- Few sellers

- Interdependent decision making

- Barriers to entry

Game Theory:

- Nash Equilibrium: Each player's strategy is optimal given others' strategies

- Dominant Strategy: Best choice regardless of what others do

- Tension between cooperation and self-interest

- Oligopolies will tend toward market equilibrium

Monopolistic Competition

Characteristics:

- Many sellers

- Differentiated products

- Free entry and exit

Behavior:

- Short run: Like monopoly (can earn profits)

- Long run: Like perfect competition (zero economic profit)

- producing where MR=MC, price will eventually = ATC, due to firms entering and exiting

- reduced market share can be viewed as a decrease in supply

- P > MC (some inefficiency)

- Excess capacity in long run

6. Factor Markets (6-12% of exam)

Derived Demand

- Input demand derives from output demand

- Marginal Revenue Product (MRP): MR × MP

- Value of Marginal Product (VMP): P × MP (in perfect competition)

- Firm hires inputs where MRP = input price

Labor Markets

- Labor Demand: Determined by MRP of labor

- Labor Supply: Determined by opportunity cost of time

- Equilibrium Wage: Where labor supply = labor demand

- Marginal Factor Cost (MFC): Cost of hiring one more worker

Factors Affecting Factor Demand

- Output price changes

- Productivity changes

- Prices of other inputs

- Technology changes

7. Market Failure and Role of Government (8-14% of exam)

Externalities

- Positive Externalities: Benefits to third parties (education, R&D)

- Negative Externalities: Costs to third parties (pollution)

- Private Value vs. Social Value: Market failures occur when they differ

- Solutions: Taxes, subsidies, regulations, property rights

- Market Efficiency: (allocative efficiency) occurs when resources are allocated to their highest-valued uses, maximizing total social welfare.

Types of Goods

| Excludable | Non-Excludable | |

|---|---|---|

| Rival | Private | Common Resource |

| Non-Rival | Club Good | Public Good |

- Private Goods: Food

- Club Goods: Software

- Common Resources: Fish in a pond

- Public Goods: Infrastructure

- Free Rider Problem: People use without paying

- Government provision necessary

Income Distribution

- Income Inequality: Uneven distribution of income across population

- Lorenz Curve: Graphical representation showing cumulative percentage of income earned by cumulative percentage of population

- Perfect equality = 45-degree line

- Greater curve from line = more inequality

- Gini Coefficient: Numerical measure of inequality (0 = perfect equality, 1 = perfect inequality)

- Calculated as area between Lorenz curve and line of equality

- Sources of Income Inequality:

- Education and skill differences

- Discrimination (gender, racial, age)

- Market power and monopoly rents

- Technological change favoring skilled workers

- Globalization effects

- Inheritance and wealth concentration

- Labor market institutions (unions, minimum wage)

Antitrust and Regulation

- Antitrust Laws: Promote competition, prevent monopolies

- Regulation: Government control of natural monopolies

- Deregulation: Removing government controls to increase competition

Formulas

Elasticity

-

Price Elasticity of Demand:

-

= Elastic -

Cross-Price Elasticity:

- Positive = Substitute

- Negative = Compliment,

-

= Strong relationship (elastic) -

Income Elasticity:

- Positive = Normal

- Negative = Inferior

Costs and Production

-

Opportunity Cost:

-

Marginal Product:

-

Marginal Cost:

-

Profit:

Consumer Theory

-

Utility Maximization:

-

Budget Constraint Slope:

-

Marginal Rate of Substitution:

Market Structure

-

Profit Maximization:

-

Perfect Competition:

-

Monopoly:

Factor Markets

-

MRP:

-

Labor Demand:

Exam

Notes Post-Exam

Write Before Starting Test

- Types of goods

- Elasticity (midpoint)

- Profit Max

- Labor Max

- Consumer Max

Problem Topics

close notes while taking practice tests to get the most out of practice

Practice test 1 (61/80)

- Tax burden

- Marginal Rate of Substitution

- Diminishing Returns start when MP starts to fall

- Opportunity Cost vs Economic Cost aka Total Opportunity Cost (Petersons 1-43)

- Economic Profit (Petersons 1-45 is asking for the wrong thing)

- Monopoly Profit-Max: Output where MR=MC, Price = Demand Curve

- Monopolistic Competition

- Cartel vs Oligopoly

- Profit Max when hiring (apples to apples)

Practice Test 2 - Marginal rate of substitution

- 27 does not include question - if he spends 32 hours writing what is his total revenue?

- 55 and 56 have no graph labels: A is demand, B is marginal revenue, C is Marginal Cost, D is Average Total Cost, Total Revenue =

and Total Cost = - ChatGPT says the answer to 48 is wrong

High-Weight Topics

- Firm Behavior and Market Structure (25-33%)

- Supply and Demand (15-20%)

- Basic Economic Concepts (10-16%)

Key Concepts to Master

- Profit maximization across all market structures

- Elasticity calculations and applications

- Consumer optimization

- Cost relationships and curves

- Market efficiency and deadweight loss

Graph Analysis Skills

- Supply and demand shifts vs. movements

- Cost curves and their relationships

- Consumer choice (budget lines and indifference curves)

- Market structures and their outcomes

Common Question Types

- Definition and application questions

- Graph interpretation

- Calculation problems (elasticity, costs, profit)

- Comparative analysis between market structures

- Policy analysis (taxes, regulations, externalities)