CLEP Financial Accounting

Table of Contents

-

[[#General Topics]]

- [[#Generally Accepted Accounting Principles (GAAP)]]

- Accounting/Transaction Analysis

- [[#The Accounting Cycle]]

- [[#Business Ethics]]

- [[#Purpose of, Presentation of, and Relationships Between Financial Statements]]

- [[#Forms of Business]]

-

[[#The Income Statement, also called Profit & Loss (P&L)]]

- [[#Presentation Format Issues]]

- [[#Recognition of Revenue and Expenses]]

- [[#Costs of Goods Sold (CGS) - also called Operating Expenses]]

- [[#Irregular Items]]

- [[#Profitability Analysis]]

- [[#Summary]]

-

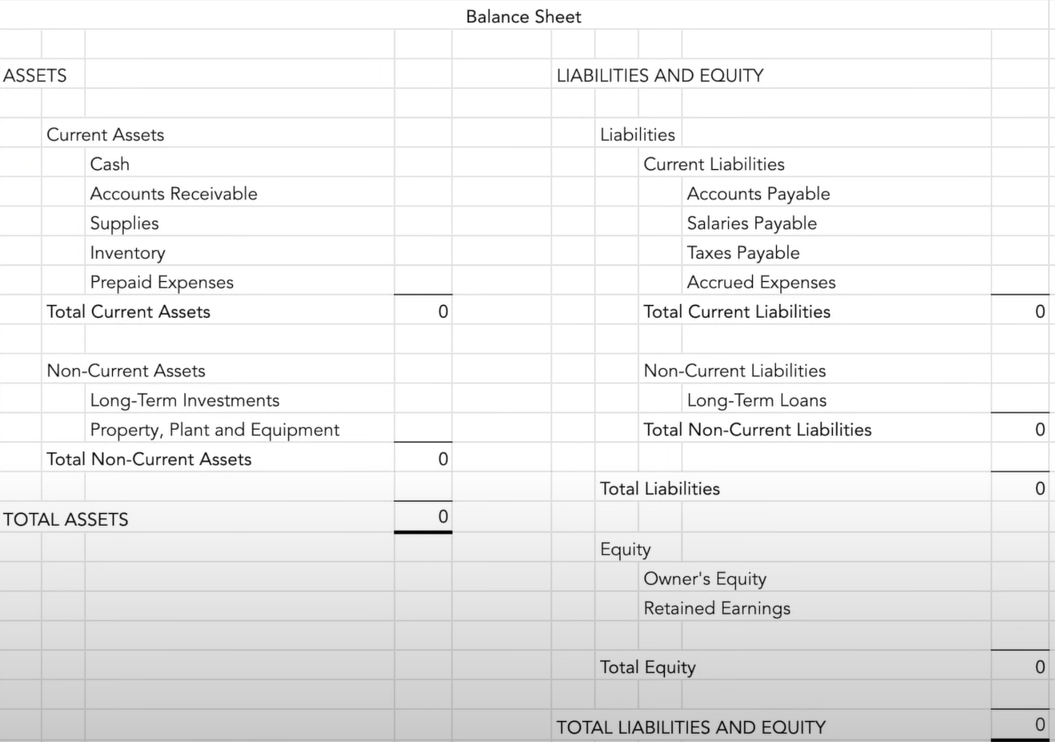

[[#The Balance Sheet]]

- [[#Cash and Internal Controls]]

- [[#Valuation of Accounts/Notes Receivable including Bad Debts]]

- [[#Valuation of Inventories]]

- [[#Acquisition and Disposal of Long Term Assets]]

- [[#Depreciation/Amortization/Depletion]]

- [[#Intangible Assets]]

- [[#Accounts and Notes Payable]]

- [[#Long-Term Liabilities]]

- [[#Owner's Equity]]

- [[#Preferred and Common Stock]]

- [[#Retained Earnings]]

- [[#Liquidity, Solvency, and Activity Analysis]]

-

[[#Statement of Cash Flows]]

- [[#Indirect Method]]

- [[#Cash Flow Analysis]]

- [[#Operations, Investing, and Financing Activities]]

-

[[#Miscellaneous]]

- [[#Investments]]

- [[#Contingent Liabilities]]

- [[#Adjusting Entries]]

-

[[#Formulas]]

-

[[#Study Notes and Tips]]

General Topics

Process Flow: Identify Transaction → Record Transaction → Post To a General Ledger → Unadjusted Trial Balance → Adjusting Entries → Adjusted Trial Balance → Create Financial Statements → Post Closing Entries

Generally Accepted Accounting Principles (GAAP)

![[GAAP.m4a]]

Created by the Financial Accounting Standards Board (FASB) - not a government entity

Purpose: Identify, Measure, and Communicate Financial Information for economic and business oriented entities and interested parties.

Primary Concern: Financial statement (reporting) regulation: Balance Sheets, Income Statement, Statement of Cash Flows, Disclosure and oversight.

Important Note: If a mistake affects a financial statement, the financial statement must be reissued after correction.

Primary Principles

The 3 primary principles are: Conservative, Going-Concern, and Objectivity

Complete List of GAAP Principles:

- Dual Entry Principle: Transactions get recorded twice for checks and balances

- Business Entity Principle: The business is treated as a separate entity

- Conservative Principle: Resolving financial statement uncertainty in the least favorable way; anticipates future losses, not gains; understates net assets and income

- Going-Concern Principle: Assume that the business will last indefinitely; allows fulfillment of obligations and objectives

- Objectivity Principle: Transactions recorded using best objective evidence; cannot make assumptions; allows accounting department from documenting slanted information; records figures and rids them of bias; nothing is left out of the books (Full disclosure principle)

- Stable Monetary Unit Principle: Assumes currency value stays the same each year

- Historical Cost Principle: Assets reported at historical cost (book or true value) at time of purchase

- Matching Principle: Expenses should be recognized when they can be matched with the revenue they generate

- Time-Period Principle: Financial activities can be divided into specific time periods; debts are to be paid within one year or one business cycle (whichever is longer)

- Revenue Recognition Principle: Revenue is recorded when it is earned, not when it is received (accrual-based accounting)

- Materiality Principle: The significance of an item should be considered when it is reported

Users and Standard Setting

Users: Investors, Creditors, Authorities who provide oversight (helps with capital allocation decisions)

Standard Setting - 4 Parties:

- SEC - Security Exchange Commission: Established to enforce accounting and reporting for public companies, enforcement authority, encourage private standard setting

- AICPA - American Institute of Certified Public Accountants

- FASB - Created GAAP

- Any other Governmental Entity (IRS, etc.)

Issues in Financial Reporting

- Politics - entities that provide oversight

- Expectation gap - public perception vs accountant opinion

- SOX - System that auditors must use to evaluate protocols in public and private firms

- Ethics - GAAP doesn't always provide an answer

Rules of Double-Entry | Accounting/Transaction Analysis | Accounting Equation

![[Rules for Double-Entry.m4a]]

Rules for Double-Entry Accounting

- Requires that all transactions get recorded twice

- Each entry is logged twice on a balance sheet

- Allows for checks and balances

- Equal debits and credits are made in accounts for all transactions (assets, liabilities and equity)

Factors that need to be monitored:

- Where the money is coming from (what account)

- Where is the money going

- Why is it going there

- Total debits will always equal the total credits and stay in balance

Rules of Transaction Analysis

Rules of Debits and Credits:

Increases:

- Assets - Debit

- Expense - Debit

- Liability - Credit

- Income - Credit

- Capital - Credit

Decreases:

- Assets - Credit

- Expense - Credit

- Liability - Debit

- Income - Debit

- Capital - Debit

Rules of the Accounting Equation

Basic Equation: Assets = Liabilities + Owner's Equity

Components:

- Assets: Things the business owns; resources used to make money (gold, cash, electronics, credit, property, etc.)

- Liabilities: Things the business owes a third party; debts often called expenses; must be paid within a year; can be paid with current assets with true value

- Owner's Equity: Things the business owes the owner(s); owner's claim on total assets

3 ways to demonstrate equation:

- Assets = Liabilities + Owner's Equity

- Owner's Equity = Assets - Liabilities

- Liabilities = Assets - Owner's Equity

The Accounting Cycle

![[The Accounting Cylce 1.m4a]]

Process: Identify Transaction → Record Journal Entries → Post Journal Transactions → Calculate unadjusted trial balance → Analyze worksheet and identify errors → Fix journal entries → Create Final Statement → Close Books

- Process of recording and processing all events which the business conducts

- Begins when a transaction occurs (selling, buying, or investing)

- Recording contains: date, details, debit/credit, balance of 0

- Accounting cycle is continual through the business cycle

- Natural period of time occurs before certain business activities tend to repeat (normally 1 year, but could be a month)

- Revenues and expenses are closed at the end of the accounting period

- Net income is transferred into earnings as the business prepares to ensure debits and credits are balanced

Business Ethics

![[Business Ethics 1.m4a]]

Ethics: Internalized standards that consider the legality of any action

Internal Controls

Policy and procedure implemented by a firm to ensure stability:

- Balances human desire and actions

- Not only for monitoring

- Allow for an increase in profit (Good ethics is profitable and reduces risk)

- Sarbanes-Oxley Act (SOX): A system that auditors must test and evaluate procedures in the workplace

Code of Ethics

- Issued by a third party on a high level (AICPA)

- Individual company should have its own company code of ethics which are documented and legally binding

Key Ethical Areas

- Law: People break the law and perform violations; violations are unethical

- Full Disclosure: Owner all the way down to staff; documentation of all assets, liabilities and equity must be accounted for

- Conflict of Interest: Business oriented, personal relationships, GAAP, bidding on a job

Goal: Accumulate earnings and profits through internal controls and proper ethical behavior

Purpose of, Presentation of, and Relationships Between Financial Statements

![[purpose, presentation and relationship between financial statements 1.m4a]]

Purpose

- Provide information about overall business performance

- Exhibit and document changes in financial position

- Total loss where the business cannot exist is called bankruptcy

- Useful for making economic decisions (important for owners, creditors and investors)

Key Statements:

- Income Statement: Shows the result of business operations over a given amount of time

- Statement of Owner's Equity: Calculates an end of period balance of owner's equity account; total claim that owners, investors, and creditors have over a period

Purpose of accounting is for a constantly conducted review

Presentation of Financial Statements

Standard Format Requirements:

- All financial statements have a three-lined heading: Company, Statement type, Time Period

- Start all computation placing numbers in the farthest right column

- To make a sub calculation, move one column left

- Draw a single line under the last number in a calculation

- Put a double underline under the final numbers (signifies net income, end of period balance, total assets, total liabilities, and owner's equity)

Relationships Between Financial Statements

- Activity Based Costing: Costs aligning with business operations

- Financial statements show: Inventory (product), Specific accounts (income and expenses), Costs of goods sold (based on product only not services), Net Income

Forms of Business

![[forms of business 1.m4a]]

Businesses are primarily categorized based on ownership:

- Sole Proprietor: Individual Owner, no partners, unincorporated; usually small business

- Partnership: An arrangement usually between two persons, all parties agree to advance together through business operations for mutual business interest; can also be multiple businesses that come together

- Corporation: Artificial person, creates corporate laws that govern actions of the business along with state laws; corporate management is very regulated and structured; largest type of business, therefore accounting principles much stricter; issuance of stock; regulations and structures are good for handling up to thousands of stockholders

The Income Statement, also called Profit & Loss (P&L)

![[The Income Statement.m4a]]

Core Formula:

- Revenue - Direct Expenses (Cost of Goods Sold) = Gross P&L

- Gross P&L - Indirect Expenses (Overhead) = Operating P&L also called EBIT (Earnings before Interest and Tax)

- Operating P&L - Interest - Tax = Net Profit

Presentation Format Issues

- Must follow GAAP principles

- Shows results of business operations over a period of time (month, quarter, or year)

- Income statement gauges growth

- Flow: Sales → Cost of goods sold → Gross profit → Operating expenses → Net income

- Net income is the core of the income statement

- Income statement explains why assets went up (growth of assets stems from business operations)

- Asset growth translates to an increase in profit

- Owners equity also grows when net income goes up

T-Account (Ledger):

- Used to alleviate formatting issues

- Keep track of the ups and downs in accounts

- Include what is taken in and what is going out (ups in one column, downs in another)

Recognition of Revenue and Expenses

- Income statement is a summary of Revenue and Expenses accounts into one single number: net income

- Revenue is an increase in assets or a return on assets

- Income and Expense accounts are actually just part of Owner's Equity

- Liabilities section: Where expenses are documented; explains why assets went down

- Expense Report: Separate financial statement outlining everything that was paid out in the period (must be relevant to the business)

- Deferred Revenues: Liabilities resulting from receiving cash prior to earning income (annuities, expected charges, taxes, or other income)

- Closing Entries: Serve to reduce revenues, expenses, and dividends to zero for the next accounting cycle

Costs of Goods Sold (CGS) - also called Operating Expenses

- Calculated for goods which are bought and resold

- Single number on the income statement

- CGS is the actual cost to the business

- Not all businesses buy and resell goods (services do not calculate Cost of Goods Sold)

- Goods sold can be processed from goods bought: Materials, Supplies, Labor, Machinery and Factories

- Ultimately CGS is documentation of overhead

Important: Do not overstate or understate inventory - documentation is key. If Ending inventory is overstated then COGS will be understated, and net Income will be overstated.

Irregular Items

Discontinued Operations:

- Large enough to amount to a business segment to be accounted for

- Usually involves a loss - will appear separately on a net of income tax on an income statement

- Both income and expenses will equal into a single number on income statement, then be reduced by either an income tax expense or income tax savings

Extraordinary Gains and Losses:

- Unusual and infrequent events

- Can be expected or unexpected

- Losses lower income taxes at a certain point, either now or later

- Business equipment is not included (that is an Expense)

- Lawsuits are not included

Profitability Analysis

Aids in developing ideas and strategies while planning and analyzing potential productivity while managing risk.

Types of Profitability Analysis:

- Horizontal Analysis: Company compares current results to a previous year

- Ratio Analysis: Company computes a ratio from various numbers on financial statements

- Vertical Analysis: Company compares a set of numbers to a key number elsewhere and analyze why numbers do or do not correlate

Gross Profit Margin is useful for evaluating profitability.

Summary

Profitability analysis allows:

- Business to forecast profitability

- Anticipation of Revenue and expenses

- Applicable to financial statements and business operations

- Sales Potential (Gross Profit Margin): 3 main elements - Customer age (needs/motivation), Geography (forecasting), Product Types (business operations)

The Balance Sheet

Largest Module in CLEP exam

Cash and Internal Controls

- Cash is generated from various sources

- Cash is an asset acquired and generated from business operations

- Internal controls must be attributed and created for compliance purposes with regulatory agencies (GAAP, FASB, AICPA, SEC)

- Internal Controls allow for an increase in profit, endorse accurate financial statements

- Good internal controls are in writing

- Legal Protection: Certain laws make owners responsible for crimes of employees if there are weak internal controls

- Accounting is separate from business operations though audits for even the bookkeepers

- Accounting is separate from custody of assets

Valuation of Accounts/Notes Receivable including Bad Debts

Valuation of Accounts Receivable

- A/R is a Control Account

- Contains the amounts that all customers owe the business

- Sell on Account: Debit to accounts Receivable and a credit to Sales Revenue

- Collect from Customers: Debit cash, credit accounts Receivable

- Accrual Accounting: Recognized expenses in the period they are incurred

- A/R Write-Off: Does not remove a customer from warning of accountability, but for tax purposes estimate uncollectible accounts

- Include an allowance for doubtful accounts like a contra-asset account

- Contra-Asset Account: Measures the decrease in the value of accounts receivable

- Accounts receivable turnover determines how quickly a firm collects cash on its credit sales

Valuation of Notes Receivable (including Bad Debts)

- Notes receivable are a current asset when they mature within one financial year

- Notes are recorded at their present value of each dollar amount, not including interest

- To discount a note is to sell a note to a bank that subtracts a discount

- Discounting gives the seller proceeds (an asset)

Components of Notes receivable:

- Face amount: The actual dollar amount

- Face interest: Interest rate on the note

- Future value: Amount borrowed + interest up to the maturity date

- Interest-bearing note: A note that contains an interest rate whose face amount is the present value, not the value at maturity

Important: Collecting a receivable does not affect total assets or net income. When estimating collectibles based on credit sales, record the full estimated expense.

Valuation of Inventories

- Inventory is a cost of ownership

- Inventory Valuation is the dollar amount associated with the items contained in a company's inventory

- Account for total inventory as well as individual amounts depending on the product sold

- Cost of items follows the objectivity principle

- Inventory valuation includes cost of materials, production, labor, and overhead

Methods of tracking inventory

- Periodic Inventory Method: Keeps track of merchandise cost at purchase and computes costs of goods sold on income statement

- Perpetual Inventory Method: Increases inventory account with every purchase and lowers inventory account with every sale

- Days in inventory: Measures the average number of days prior to sale, allows better projection

- Inventory Turnover: Measures the number of times inventory sells out annually

Inventory Accounting Methods

- First In First Out (FIFO): Measures the cost of inventory on a balance sheet, represents the inventory that was most recently purchased; takes the oldest items and records their sales first, even if they were never sold

- Last In First Out (LIFO): Most recently purchased items are recorded first; GAAP approved but not allowed outside the U.S.; in a period of rising prices, LIFO will result in the highest cost of goods sold

Important: Expenditures are charged to an asset account if they: Extend the life of the asset, Increase productivity or efficiency, or add significant value to the asset. If an expenditure only maintains the asset or returns it to working order, it should be expensed.

Acquisition and Disposal of Long Term Assets

Acquisition of Long Term Assets

- Also known as plant assets, capital assets, or fixed assets

- Have a life longer than one year

- Allow for the transaction of capital

- Help a business or person make money

- An asset is termed capitalized when it is changed into another asset that helps the business make money

Disposal of Long Term Assets

- If a fixed asset has passed its useful life it must be removed or replaced

- If a long-term asset is below the break even point and does not produce a profit, the business must get rid of it

- A journal entry must be made for "asset disposal" where the fixed asset is credited and the accumulated depreciation is debited

- Book Value (BV): The historical cost of a value with less accumulated depreciation

- Asset Depreciation: An asset becoming less desired after time; according to the matching principle, the expense is matched to the revenue it helps generate

- Gains and Losses are recorded on the balance sheet

Depreciation/Amortization/Depletion

Accumulated Depreciation, Amortization, and Depletion are contra-asset accounts which get subtracted from their respective asset accounts. All 3 are monitored with schedules (usually monthly).

Depreciation

- Fixed, tangible assets will depreciate

- Used bit by bit over a long period of time

- In accrual accounting we recognize the expenses as they are incurred by spreading out the expense through the life of the asset via depreciation

- When the asset is bought it is capitalized (cost recorded as a fixed asset in the balance sheet rather than an expense in the income statement)

To depreciate an asset properly you should know:

- What the asset is

- Which depreciation method you will be using

- The Asset Cost

- How long the useful life is

- What the salvage value might be after the useful life

Depreciation schedule shows:

- Opening book value (Asset value at the start of the period)

- Depreciation expense (throughout the period)

- Accumulated depreciation (total)

- Closing Book Value (Current Asset Value)

Important Notes:

- Depreciation is not an attempt to show a decline in the value of assets (some assets may actually appreciate)

- Businesses depreciate all fixed assets except land, every year

- Depreciation is not money set aside to replace aging assets

Amortization

- The amount an Intangible asset is used up during the financial period

- Amortization is an Expense

- Calculated using the asset's expected useful life

- The credit for Amortization lowers Intangible assets in the asset ledger

- There is no accumulated amortization amount (as opposed to depreciation)

- To be fully amortized, an Intangible asset's total cost will have been allocated to past fiscal periods

Depletion

- Complete letting go or selling off of major assets

- The amount of used up natural resources during the financial period

- Depletion is an Expense (you are taking a loss)

- Natural resources allow long-term projection

- Book value when fully depleted is 0

EBITDA - Earnings Before Interest Taxes Depreciation and Amortization: Provides a clear view of a company's operational performance.

Intangible Assets

Something that is definitely an asset, but has no physical form.

Examples: Patents, trademarks, loans, partnerships, branding, knowledge, goodwill, legal fees, designing, artwork, engineering, software, contracts, marketing programs, creativity, and ideas.

Specific Types

- Patents: Exclusive right to produce and sell an invention; legal right may be up to 20 years; useful life may be even shorter

- Copyrights: Exclusive right to publish, perform, or reproduce music, art, film, books, or software

- Trademarks and trade names: Special identifications protected against infringement; can have definite or indefinite lives

- Goodwill: Extra cost a business pays for another business as recognition for being unusually profitable; has an indefinite life

- Franchises and Licenses: Contracts or government grants that give the owner special rights; many have indefinite lives

Important Notes:

- Legal life of an Intangible asset can be more than 100 years, but the useful life is often much shorter

- An intangible asset is separate from a capital asset

- Total cost of an Intangible asset is everything necessary to make it useful

- If the life of an asset is known, cost is spread over the asset's useful life, not legal life

- Some Intangible assets have an indefinite life - these are not amortized

- Non-Disclosure Agreements are used to protect Intangibles

Accounts and Notes Payable

Accounts Payable

- A/P is a liability account for obligations to pay for goods or services

- Cash is credited, and accounts payable is debited

- Due to accrual accounting, accounts payable is credited even though no cash changed hands

Notes Payable

- N/P is a liability account for payment on a note when a business or person borrows money

- Promissory note: In writing states a promise to pay back the money in the future with a specific date

- Notes may or may not contain interest

- The amount borrowed itself is the principal (separate from interest, also called Present Value)

- Once paid monthly or in full, the capital must be credited on the balance sheet and ledgers

- A note can be defaulted on (stopped payments)

- Once a note is defaulted, the bank will charge the business for the maturity value, not the present value of the note plus a default fee

- A dishonored note has no value

Long-Term Liabilities

- Liabilities possess separate and important sections on financial statements

- Credits are stored in liabilities section often broken down into accounts like "Deferred warranty revenues, as current" and "Deferred warranty revenue, as long-term"

- Long-Term Liability credits will move to revenue section as deferred

Bonds

Bonds are a long-term liability and a way to borrow large amounts of money from a large amount of people.

- Face value of a bond is often different from the actual cash proceeds because the stated rate of the bond is different from the market or effective rate

- Stated rate is the cash payments for the bond (stays the same each year = stated rate × face value of the bond)

- Market value is what someone can receive for a similar bond

- Discount or premiums account for the difference in stated rate and market rate

- If your bond offers a lower rate you have to issue the bond at a discount

- If your bond offers a higher rate you can offer a premium for the bond

- Through the life of the bond you will amortize the discount/premium of the bond

Bonds payable follows 4 steps:

- Corporation prints up a number of paper bonds

- Corporation sells the bond

- Corporation makes regular cash payments on the bonds

- On the maturity date, corporation pays the bondholder the face amount

Types of Bonds:

- Treasury bonds (T-Bonds): Government bonds

- Municipal bonds: Offered by state and local government

- Corporate bonds: Bonds sold by corporations

Important Formulas:

- True Liability (Book Value) = Bond Payable - Discount

- For a premium bond, the amount of annual interest expense will be less than the amount of interest paid annually in cash

- When bonds are issued at a discount, the company receives less cash than the face value, but still pays interest on the full face value

Owner's Equity

- Official name for the Owner's claim on the assets in the business (not including creditors, but investors are included)

- Large part of the balance sheet and accounting equation

- There is a separate financial statement titled "Statement of Owner's Equity" which contains net income from the income statement over the same period of time

- Important: You can never move information between statements that do not cover the same period of time

Preferred and Common Stock

Stocks are recorded in the "Stockholder's Equity" section of the balance sheet.

- Treasury stocks: Shares the corporation has repurchased from shareholders; a contra-equity account that reduces total Stockholder's Equity; not an asset or liability

- Net Assets is what Stockholder's equity represents on the balance sheet

Preferred Stock

- Stock with dividends set at a certain percentage

- Preferred stockholders cannot make more than this set rate (rest goes to common stockholders)

- Commonly has a steady price; doesn't go up when corporation does well, doesn't go down much when company does poorly

- Preferred stockholders usually do not get to vote in stockholder meetings

Privileges preferred stockholders may have:

- First right to cash dividends before Common stockholders

- Right to participate in corporate profits the same as common stockholders

- Right to be paid dividends in arrears if years go by without paying a dividend

- Right to convert preferred stock into common stock

Common Stock

Every corporation must have common stock. Common stock represents the basic ownership of a corporation.

Rights granted to common stockholders:

- Right to vote

- Right to share in dividends (this is where investments make money)

- Right to a certain percentage of corporation upon total liquidation

- The Preemptive right: The choice to buy a portion of each new issuance of stock to maintain the same ownership percentage

Corporations can offer Class B common stock which may have more or less voting rights.

Retained Earnings

- Located in the equity account

- Retained earnings contain all the earnings the corporation has ever earned, all assets, returns on investments, and all other revenue

- These earnings have not yet been distributed to stockholders

- Investors and creditors will not be paid until Retained earnings are documented

Liquidity, Solvency, and Activity Analysis

Usually the term analysis refers to a ratio.

Liquidity Analysis

- Liquidity is the ability of a company to meet its financial obligations as they come due

- Analysis of liquidity is a measurement of a company's ability to pay short-term debts

- If a company is having trouble meeting its short-term debts, it is at a higher risk of bankruptcy

- A very liquid company could have too much liquid cash, or need too much cash

Solvency Analysis

- Solvency is the ability of a company to meet its long-term financial obligations

- A low Solvency ratio means a greater probability that a company will default on debt obligations

Activity Analysis

- Activity Analysis is an examination of activities involved in producing goods or services to better understand and manage costs

- Includes identifying factors that drive costs (often called "Activity Drivers")

- Tool to measure the ability of a business to alter various assets, liability, and capital accounts into revenue creating a capital surplus

- The faster a business is able to convert its assets into revenue, the smoother it will operate

Statement of Cash Flows

Exchanges of cash require a separate statement per federal law. All cash must be documented in more detail than any other type of currency.

The Statement of Cash Flows is broken into three main parts:

- Operating Activities: Day to day business operations (revenues and expenses)

- Investing Activities: Buying or selling long-term assets (investments, land, equipment)

- Financing Activities: Borrowing money, Repaying loans, or Issuing stocks and bonds

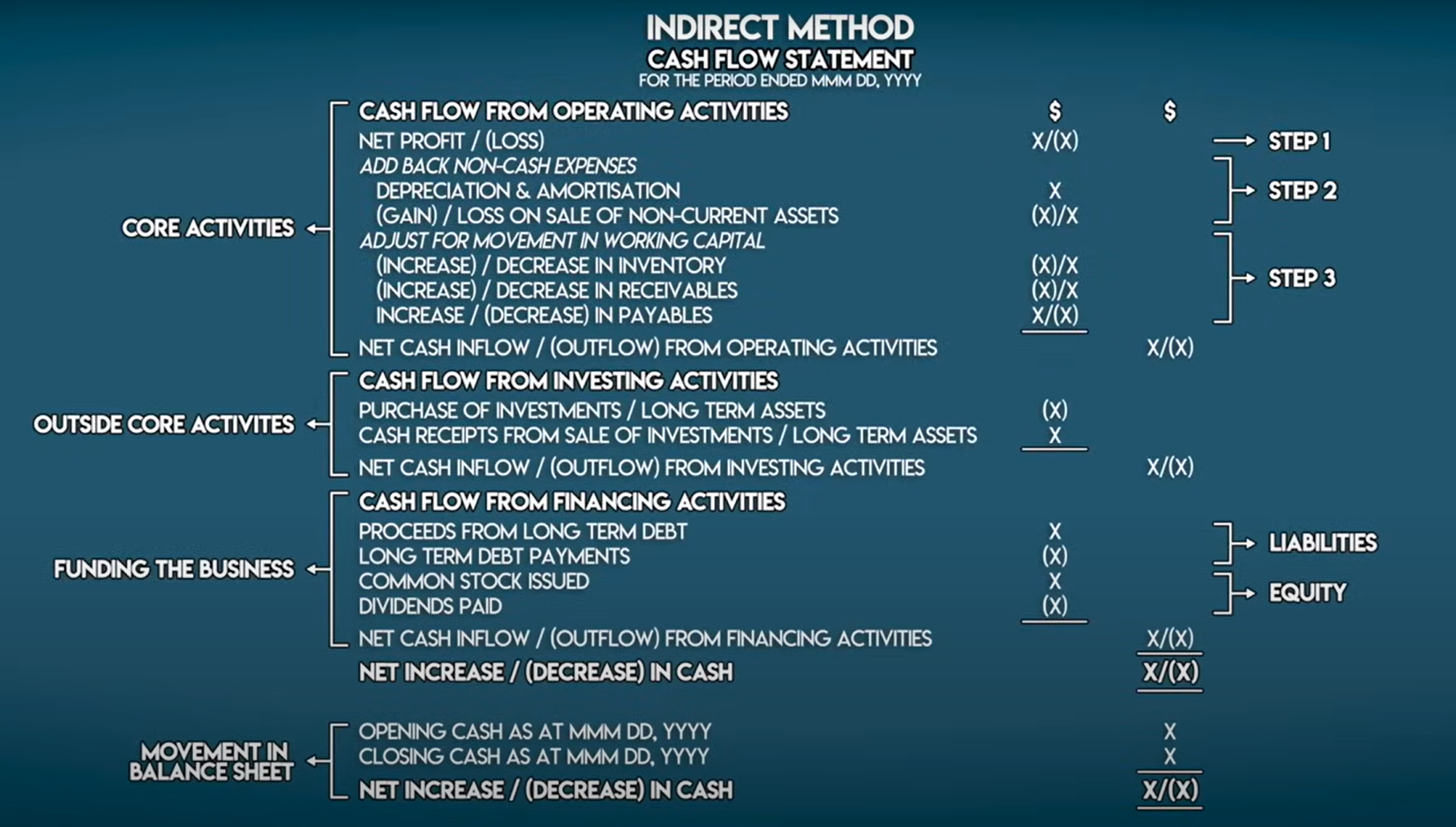

Indirect Method

The Indirect Method is the usual method of computing cash flow from business operations.

- Starting with net income (take home after expenses) on the cash flow statement

- Uses the changes in the asset and liability accounts to adjust net income

- Because expenses and revenues have been credited and debited respectively in the calculation for net income, in the statement of cash flow they are inversed (revenues are credited/subtracted and expenses are debited/added)

- This adjustment allows for net income to transfer into "Cash Flow From Business Operations Activity"

- By adding total net cash flow to a beginning cash account balance we get the value for "cash-end of period"

- This number must equal the balance in the cash account at the end of the financial period

Cash Flow Analysis

- Analysis of a company's cash inflows and outflows to understand its financial health and ability to meet obligations

- Utilized for reporting purposes in the cash flow statement

- Shows where the cash came from and where it went during the period

- Cash Flow is displayed from: Operations, Investing (including land and property), and Financing (debits and credits)

Operations, Investing, and Financing Activities

Operating Activities

- First section of the Statement of Cash Flows

- Operations is what a business normally does to make money

- Interest paid also goes in this section

Investing Activities

- Second section of the Statement of Cash Flows after Operating Activities

- Displays business' income-producing sources mainly: Long-term investments, Land, and Equipment

- Normal to observe a negative number on the investment section as investments vary in price and land/equipment are often expenses that generate revenue

- Investing Activities signify that cash went out of the company to purchase assets

Financing Activities

- Third section of the Statement of Cash Flows after Investing Activities

- Includes cash flows related to the company's own capital and debt activities

- Money returned to investors is also reported, called Loan payable

- This is where the money is paid to the principal on a loan from a lender

Miscellaneous

Investments

- If a business has means, it will invest to produce a return (ROI)

- Investments are uses of a business' money to buy assets, to make more money and buy more assets

- Long-term investments: Assets like property, land, equipment, or investments in other businesses

- Held-to-Maturity investments: Long-term investment that businesses do not intend to sell

- Short term investments: Usually have a lower ROI (Certificate of deposit (CD), Stock)

- Trading Investments: All considered public, more regulated

- Available-for-Sale Investments: All considered private, less regulated

Contingent Liabilities

Potential and unknown cost that may or may not incur.

Three Categories:

- High Probability: The costs can be estimated, however a loss must be disclosed in statements (i.e. property purchased)

- Medium Probability: The cost must be disclosed if the contingency is probable

- Low Probability: Very unlikely but still disclosed on financial statements

Adjusting Entries

When transactions span accounting periods, an adjusting entry is needed to bring things in line with the accrual method of accounting.

Incurred - become subject to. Accrued - accumulate

Prepayments

Payment in the past, exchange of goods/services in the future.

Prepaid Expense - Deferred expense

- A future expense which has been paid for in advance

- At payment cash is credited, expense is debited

- Adjusting Entry (before benefit): Expense is credited (Income Statement), Prepaid Expense asset is debited (balance sheet)

- Adjusting Entry (after benefit): Expense is debited, Prepaid Expense is credited

Deferred Revenue - Unearned Revenue

- Adjusting Entry (before earned): Debit Cash, Credit Liability (Deferred Revenue)

- Adjusting Entry (after earned): Debit Deferred Revenue, Credit Revenue (income statement)

Accruals

Goods/services are to be invoiced in the future. Goods/services are provided in the past on credit.

Accrued Expenses

- You are the buyer, you have received but not paid

- Adjusting Entry (before billed): Debit Expense, Credit Liability (accrued expense)

- Adjusting Entry (after billed): Debit Expense, Credit Accounts Payable

- Release Accrued Expense: Debit Accrued Expense, Credit Expense

Accrued Revenue

- Unbilled Revenue (You are the seller)

- Adjusting Entry (before billed): Credit Revenue, Debit Accrued Revenue (asset)

- Adjusting Entry (after billed): Debit Accounts Receivable, Credit Accrued Revenue

Formulas

Formula 1: Accounting Equation

Alternative forms:

Formula 2: Cost of Goods Sold (COGS)

Formula 3: Gross Profit

Formula 4: Gross Profit Margin (Sales Potential)

Formula 5: Allowance for Uncollectible Accounts

Formula 6: Working Capital

Formula 7: Net Accounts Receivable

Formula 8: Days' Inventory on Hand

Formula 9: Gain or Loss on Disposed Asset

Formula 9 (Alternative): Bond Interest Expense

Formula 10: Net Assets

Formula 11: Retained Earnings

Formula 12: Liquidity Ratios

Current Ratio:

Quick Ratio:

Formula 13: Solvency Ratio

Formula 14: Cash Flow Statement

Exam Notes and Tips

Exam Information

- 75 Questions in 90 Minutes

- 25% General Topics

- 25% The Income Statement

- 35% The Balance Sheet

- 7% Statement of Cash Flows

- 3% Miscellaneous

Key Study Areas (Based on Student Feedback)

Critical Areas to Master:

- All Formulas - Memorize and write them down at the start of the exam

- Debits and Credits - Use the D.E.A.L.E.R method:

- Debits: Dividends, Expenses, Assets (increases)

- Credits: Liabilities, Equity, Revenues (increases)

- Journal Entries and Adjusting Entries (AJE)

- Contra revenue accounts

- Quick ratio formula

- Bank Reconciliation (deposits in transit, outstanding checks, etc.)

- Financial ratios (Current Ratio, Quick Ratio, Debt-to-Equity Ratio)

Important Topics:

- Internal Controls

- Extraordinary items

- Cost of goods vs Cost of Sales

- Net Purchases calculation for COGS

- Journaling bad debts, prepaid expenses, and unearned revenue

- Stock dividends (fair value and equity method)

- When to record an expense/revenue

- Bad debts and allowances

- Different inventory valuation methods (FIFO, LIFO)

- Depreciation and amortization (3 main formulas: straight line, double declining, units of production)

- Cash flows categories (operating, investing, financing)

- Cash basis vs accrual basis

- Direct vs indirect cash flows

- Account classifications (Assets, contra-assets, Liabilities, contra-liabilities, Equity, contra-equity)

GAAP Concepts to Know:

- Objectivity

- Going concern

- Conservatism

- Cost (historical cost)

- Materiality

Useful Resources

Practice exams available at:

Additional Study Links

Excalidraw Data

Text Elements

Beginning inventory

- Net Purchases

- Ending Inventory

= Cost of Goods Sold

Sales

- Cost of Goods Sold

= Gross Profit

Assets

- Liabilities

= Owner's Equity